Der Beitrag ecosio Insights: E-invoicing Mandates and the Growth of B2B Process Automation erschien zuerst auf ecosio.

]]>To explore the latest trends and challenges in this space, we sat down with ecosio ‘s E-invoicing Product Manager, Chris Newman. In this interview, Chris shares his expert insights into the future of e-invoicing, including how businesses can prepare for upcoming e-invoicing mandates, the role of emerging technologies, and the importance of global cooperation in shaping the future of electronic invoicing systems.

————————————————————————

How do you expect e-invoicing to evolve over the next few years?

The global e-invoicing landscape is undergoing significant transformation. In addition to a continued expansion of e-invoicing mandates, one key trend I expect to continue is the adoption of Continuous Transaction Controls (CTCs). These help governments to combat VAT fraud and tax evasion by requiring real-time or near-real-time reporting of the invoice or a subset of transactional data to central platforms.

I also expect interoperability to become a key concern, as more countries mandate electronic invoicing across B2B, B2G, and B2C transactions. This trend is driving the adoption of global standards and frameworks such as Peppol, which facilitates seamless cross-border transactions and ensures compliance with varying national requirements.

Last, but not least, we should see the integration of e-invoicing with broader compliance initiatives, such as e-transport systems, which track the movement of goods to ensure accurate VAT reporting and delivery verification. Countries like Romania, Serbia, and Hungary are already implementing these systems, and I expect others to follow as we move towards more comprehensive compliance frameworks.

Will emerging technologies have a role to play in e-invoicing processes moving forward?

New technologies will undoubtedly play a significant role in enhancing e-invoicing processes moving forward. At ecosio, for example, we are already leveraging AI to enhance our solutions and reduce risk for clients. Meanwhile, governments are also recognising the potential for AI to optimise compliance processes, with some already using AI to identify fraud that would previously have taken weeks to uncover. As is always the case with integration of AI, however, it must be managed carefully if accuracy is to be maintained.

Transitioning to cloud-based solutions is also transforming how businesses handle e-invoicing. Modern cloud architecture offers scalability, instant accessibility and capacity for real-time processing, providing seamless integration between financial systems and enhancing transactional transparency.

Do you anticipate that governments will expand B2B automation requirements beyond invoicing processes?

Yes, I think this is certainly going to happen in many countries moving forward. In fact, several countries have already made progress in this direction. For instance, the United Kingdom, besides e-invoices, also mandates electronic purchase orders and advanced shipping notices for medical suppliers engaging with healthcare providers. Similarly, Italy mandates the use of electronic purchase orders in the public healthcare system.

As already mentioned, e-transportation initiatives are also on the rise, which involves the monitoring and tracking of high fiscal goods during transit. Therefore we can expect to see more countries introducing their own initiatives.

Is there any hope for a universal e-invoicing standard?

It’s certainly true that we’re heading in the right direction. Standards like EN 16931, initially developed for B2G invoicing under EU Directive 2014/55, are now expanding into the B2B sphere across Europe and even countries like Saudi Arabia, United Arab Emirates, Singapore and Australia. Similarly, interoperability frameworks such as Peppol are gaining significant traction. However, full global alignment remains highly improbable due to proven, established systems that have been in place for a long time, which is the case in Latin America. While e-invoicing may become more unified in some regions, we won’t see a universal standard emerge any time soon.

What role will global cooperation play in the further development of e-invoicing?

If e-invoicing is to become as simple and efficient as possible, global cooperation is essential. While developing a system specifically to tackle local needs may have seemed logical for the first countries to implement mandatory e-invoicing, this quickly led to fragmentation and overly complicated cross-border transactions.

Thankfully, however, recent years have seen significant steps taken towards international cooperation. In particular, initiatives like the EU’s VAT in the Digital Age (ViDA) and the Peppol International Invoice (PINT) exemplify the potential of collaboration. By adopting the EN 16931 standard, ViDA aims to harmonise digital reporting across the EU, facilitating seamless cross-border transactions while enhancing automation and reducing administrative burdens for businesses. Meanwhile, PINT bridges global standards with local requirements, as demonstrated by its adoption in countries such as Japan (PINT-JP), Malaysia (PINT-MY), Singapore (PINT-SG), and Australia & New Zealand (PINT-A-NZ). These efforts not only promote efficiency but also highlight the necessity of international alignment to ensure the sustainable development of e-invoicing systems worldwide.

What are the biggest challenges businesses face when integrating and upgrading e-invoicing systems?

One of the primary challenges is being able to extract the required information from multiple systems. Many multinational organisations utilise a variety of ERP systems, which makes data identification and retrieval extremely difficult. Once the data is located, businesses must generate compliant invoices and establish connections with solution providers capable of handling requirements and meeting e-invoicing mandates across multiple markets.

Another major challenge is ensuring the data meets the necessary quality standards for these systems to function effectively. While solution providers can help to some extent here, issues concerning data quality will require significant internal commitment to resolve.

What lessons can businesses learn from early adopters of e-invoicing systems?

From what I have seen, one of the most crucial mistakes businesses make when implementing an e-invoicing solution is failing to assemble a cross-functional team with expertise in IT, finance, and tax. Without the input of experts in each of these areas, projects are much more likely to encounter challenges down the line.

Many early adopters – particularly those operating cross-border – also underestimated just how complicated managing e-invoicing internally would become, as e-invoicing mandates grew steadily more numerous and complex. Thankfully, partnering with a specialised solution provider can alleviate much of the burden, from handling country-specific connectivity requirements to ensuring compliance with technical specifications.

How important is employee training in the successful implementation of e-invoicing?

It’s crucial! While solution providers like ecosio manage most e-invoicing processes, businesses must ensure their internal teams have the expertise to manage responsibilities within their ERP systems. This includes understanding required data fields, output formats and transmission protocols like APIs or AS4.

Trained employees are also essential for managing e-invoicing workflows and addressing unique use cases. Without this internal knowledge, businesses may face significant challenges during implementation and will find it much harder to achieve long term success.

Do you have any advice for managing the increasing complexity of e-invoicing mandates?

My first recommendation would be to prepare for upcoming e-invoicing mandates and requirements as soon as new regulations are announced… if not before! Implementation of a new solution can be a lengthy process, particularly for larger companies with multiple ERP systems. Plus companies also need to understand technical compliance demands and build a capable project team. Proactively adapting systems in advance of upcoming mandates not only eliminates the danger of non-compliance penalties, which can be very severe in some jurisdictions (such as jail time for CEOs in Malaysia), but also provides a competitive advantage.

My second recommendation would be to invest in external e-invoicing expertise. As more and more countries introduce e-invoicing mandates, it is becoming increasingly unrealistic for internal teams at multinational companies to stay on top of constantly changing requirements. External providers can prove invaluable in helping to minimise risk and futureproof e-invoicing processes.

Der Beitrag ecosio Insights: E-invoicing Mandates and the Growth of B2B Process Automation erschien zuerst auf ecosio.

]]>Der Beitrag How to Manage the Growing Challenges of Tax Reporting, B2B integration and E-invoicing erschien zuerst auf ecosio.

]]>- Tax reporting is becoming more complex due to diverse national regulations and frequent legislative changes, requiring adaptable solutions

- B2B integration demands the ability to connect with multiple systems, formats, and protocols while maintaining data accuracy and process efficiency

- E-invoicing compliance involves meeting varying legal requirements, integrating with ERP systems, and handling real-time reporting obligations

- ecosio enables seamless data exchange, ensures compliance with country-specific regulations, and reduces the internal effort needed for integration and reporting

To the objective observer, modern B2B transactions are faster, more secure and more detailed than ever. Yet this constant drive towards efficiency is only partly due to organic process improvement within these organisations. Another key piece of the puzzle is the growing maze of mandates covering everything from tax reporting to logistics documents such as waybills and e-invoices.

Despite being largely responsible for the speed of improvement of B2B payment processes worldwide, increasingly complex requirements are becoming an issue for many businesses.

With governments around the world tightening regulations and increasing their focus on transparency, companies today are under growing pressure to meet stringent requirements that often seem to pull them in conflicting directions. At the same time as being required to prioritise accuracy and data visibility to comply with new tax responsibilities, businesses are also required to adapt their systems to accommodate new electronic invoicing regulations. Meanwhile, there’s also a constant internal push to expand automation in order to improve efficiency.

As a result, many organisations find themselves struggling to keep up, unsure of how to manage the intersection of these key areas.

In this article, we’ll explore the implications of this situation and discuss strategies for effectively balancing compliance and automation moving forward.

Before we discuss the relationship between compliance and automation, however, let’s first look in a bit more detail at the recent explosion of mandates across these areas…

The growing governmental appetite for data

In recent years we’ve seen a significant shift in how governments worldwide approach tax collection. CTC mandates are popping up at a rapid pace, driven by a hunger for real-time data. No longer are governments content with just the basic information; they want to know every detail about every transaction.

By far the clearest evidence of the growing appetite for data over the past decade is the pace at which countries across Europe and beyond have introduced e-invoicing requirements for various types of transaction. The start of this wave can be traced back to the passing of the EU Directive 2014/55/EU on 16 April 2014, which set deadlines for invoice recipients in public tenders to be able to accept e-invoices. Since then, many countries have gone much further – extending e-invoicing requirements beyond B2G connections to many (and sometimes all) B2B transactions.

But the hunger for data doesn’t stop at invoicing. We’re already seeing signs that the same will happen for logistics processes, with Romania, India, and Turkey having recently introduced waybill systems. When looking at B2G processes, we also see a trend towards electronic purchase orders, particularly in the Scandinavian countries. Since B2G often paves the way for B2B mandates afterwards, we are quite likely to see electronic purchase orders becoming part of future mandates.

Realistically, it’s only a matter of time before the need for detailed, real-time data becomes the norm across all aspects of business transactions.

Why is the demand for data growing?

To understand why there’s such a growing demand for data, we need to take a step back and look at the bigger picture. Taxation, at its core, is a means for governments to collect revenue for public services. But to ensure that taxes are being accurately assessed and collected, there needs to be a robust system in place for verifying the legitimacy of the transactions on which these taxes are based.

This is where data comes into play. To determine if the tax associated with a delivery of goods or services is legitimate, one needs to follow the audit trail of that transaction. This means not only looking at the invoice but also cross-checking it against the associated delivery and order documents.

For example, if a company reports an invoice for a delivery of goods, rather than taking the invoice at face value, the tax authority often verifies that the goods were actually delivered and that the terms of the invoice match the original purchase order. Such validations usually happen on a random sample basis post audit.

In order to allow for a real time verification and accurate cross-referencing of invoice documents against the underlying purchase order and delivery documents, authorities will need to have relevant information available in real time on their side. The following figure shows the concept of data reconciliation between an invoice document and an underlying purchase order and despatch advice document.

Consequently further mandates requiring delivery and purchase order information to be made available to the authorities (such as the recent waybill mandates in Turkey) are likely to be implemented more widely. Similarly, China also offers a useful window into what the future may hold here. Instead of managing tax collection through an invoice document, China wants to manage tax through big data. While data protection and legal regulations might prevent such an extensive approach in most countries, the direction in which tax collection is heading is clear.

But the push for greater data transparency is about more than just ensuring accurate tax collection. The recent tidal wave of e-invoicing mandates was principally inspired by a desire to combat fraud and reduce the shadow economy (as evidenced by the rigour with which the EU is tracking the reduction of the VAT gap). By requiring businesses to submit detailed, real-time data, governments can more easily detect suspicious activity, such as underreporting of sales or over-inflating expenses. In this way, the growing demand for data serves as both a revenue assurance measure and a tool for maintaining the integrity of the tax system.

The graph below shows the difference between the VAT gap in EU countries between 2020 and 2021:

Source: https://taxation-customs.ec.europa.eu/system/files/2023-10/VAT%20Gap%20Report%202023_0.pdf

What does the future hold?

As we’ve already touched on, the future of tax reporting and data collection is likely to see an even greater emphasis on detailed, real-time data. When we examine the current trends in international mandates, it’s clear that governments aren’t just content with capturing invoice data. They’re also increasingly interested in data relating to logistics and ordering.

“Peppol was not built as simply a tool to streamline e-invoicing, but rather as a comprehensive network infrastructure. All the technologies necessary to fulfill further mandate requirements covering purchase orders and dispatch advice messages are already there ready to be used.”

Philip Helger

Over the coming years it’s very likely that we’ll start to see mandates covering a wider spectrum of B2B communications. In particular, it seems logical that submitting purchase orders and logistics documents in real-time will become a requirement in many countries, as this would allow tax authorities to have a complete picture of a transaction, from the initial order right through to the final delivery.

What does this mean for businesses?

If current trends continue as expected, not only will businesses need to be prepared to handle a growing volume of data, they’ll have to ensure this data is accurate, easily accessible and archived appropriately.

Specifically, businesses need to get the following three things right:

- VAT – This is particularly important for cross-border and triangular transactions

- VAT reporting – This is complicated by the fact that every country’s rules are different

- E-invoicing – This involves both technical and functional challenges, including collecting data points properly in the ERP system, realising the transmission to the authorities, and getting government issued IDs back

Further, businesses will also need to invest in robust digital infrastructure that can support real-time data exchange and integrating systems across the supply chain.

Understandably, all this work can seem like a big headache – particularly when tight deadlines are involved. However, new data regulations also bring opportunity for businesses. Approached correctly, tax and e-invoicing mandates can act as a catalyst for positive change and an opportunity to align tax reporting with broader automation efforts.

“Rather than seeing upcoming regulations as a headache, businesses would do better to approach them as an opportunity to enhance system efficiency and data accuracy in the long term.”

Philipp Liegl

Why are so many businesses struggling?

One of the core reasons that many modern businesses are struggling to juggle compliance and automation requirements is that, historically, tax and EDI/e-invoicing have been viewed as entirely separate domains, each with its own set of objectives and mindsets. This siloed approach has led to inefficiencies and confusion as businesses attempt to integrate these areas to meet modern regulatory standards.

Furthermore, many companies still have limited experience when it comes to e-invoicing. In Germany, for example, companies which only do business with German suppliers and customers have not yet been subject to any e-invoicing regulations. Even with large multinationals trading in various different jurisdictions, the ownership of the e-invoicing process has so far been left to the local entities – e.g. Italy and Spain – without any central governance or ownership.

The traditional tax mindset

In the tax world, as a speaker at a recent tax conference put it, “the key goal is to stay out of prison!”. While all good tax compliance service providers naturally seek to improve process efficiency, innovation and development in this direction is driven by two key factors: the need to meet changing compliance requirements, and the desire to perfect tax process accuracy. Although tax engines and tax determination add-ons for ERP systems have greatly improved this process over recent decades, tax has largely remained a company-internal function. With the advent of e-invoicing this has changed, as many different technical requirements (e.g. exchange formats and exchange protocols) need to be taken into account. This typically falls outside the area of expertise of internal tax personnel.

The traditional EDI mindset

By contrast, for professionals working with Electronic Data Interchange (EDI) and e-invoicing, automation and data exchange with external parties has long been a central focus. Document standards like EDIFACT or ANSI ASC X12 and exchange protocols like AS2, OFTP2 or X.400 have had a significant impact in improving automated communication between different business partners along the supply chain. These technologies were developed to reduce manual intervention, improve speed, and minimise errors in data exchange, leading to more efficient business processes. Although accuracy is obviously still crucial in EDI/e-invoicing, the principal goal of these areas has historically been to improve efficiency and reduce operational costs of supply chain processes through automation. While the invoice is certainly a part of supply chain processes, it is only one document. The majority of exchanged documents in supply chain processes are logistics documents, such as purchase orders, purchase order responses and despatch advice messages.

Are B2B integration, e-invoicing and tax reporting really that different?

At first glance, B2B integration, e-invoicing and tax reporting might seem like three totally distinct areas, each with its own processes and requirements. However, when you look a little closer, they’re very closely related indeed.

In a nutshell, EDI (the core of modern B2B integration) is a methodology utilised by organisations to exchange business documents such as purchase orders, shipping notices and electronic invoices (among others) with one another in a standardised electronic format. E-invoicing, meanwhile, effectively refers to the exact same process, just relating solely to one type of document, the key difference being that the required data points and standards for e-invoices are typically dictated by the government. In addition, in many jurisdictions the invoice documents are not exchanged between the business partners directly, but via a central service provided by the government.

Similarly, there is a huge overlap between tax reporting and e-invoicing. An invoice, after all, is a record of a transaction, and that transaction is directly tied to the taxes that should be collected.

Ultimately, while there are still differences between these areas, the overall trend is clear: B2B integration, e-invoicing, and tax reporting are becoming more intertwined, and thinking of these areas as islands is no longer helpful.

Governments are increasingly demanding not just invoices but also logistics documents and other transaction-related data. Further, in several jurisdictions official government-issued information must now be brought back to the ERP – usually via dedicated APIs. For example, in some countries with CTC mandates, businesses must submit invoices in a specific XML format through a Web Service, with the state in turn providing an official invoice approval number to confirm the legitimacy of the transaction. That official approval number must be stored in the ERP system in order to be available in case a credit note is issued for the invoice (e.g. in case the invoice is being cancelled). In such cases the official approval number of the state must be part of the credit note.

As processes such as this become more commonplace, businesses will need to adapt to a landscape where EDI, e-invoicing and tax reporting are no longer distinct processes, but part of a unified approach to managing business communications and compliance. This will require a shift in how companies approach their digital infrastructure, with a focus on integrating these processes to ensure seamless data exchange and compliance.

The benefits of a unified solution

Given the growing demand for data and the increasingly blurred lines between B2B integration, e-invoicing and tax reporting, having a single provider who can handle all these related issues offers several significant advantages, including…

- Stress-free compliance. As tax, B2B integration and e-invoicing regulations continue to accelerate and overlap, having a provider that stays on top of country-specific requirements and proactively implements the necessary updates will become increasingly valuable.

- More time for internal teams. Handing key B2B integration, e-invoicing and tax reporting tasks to an external solution provider greatly reduces the strain on internal teams. With more time, individuals can then focus on more value-adding activities and initiatives.

- Reduced vendor complexity. With a single provider managing your B2B integration, e-invoicing and tax reporting, the administrative burden of juggling multiple platforms and processes is lightened. This saves time, reduces the risk of errors, improves data visibility, and makes system integration much simpler. What’s more, when issues do arise, there’s no need to jump between different support portals.

- Cross-functional expertise. With a unified B2B integration, e-invoicing and tax reporting solution you get a partner that understands the complex overlaps between these areas and can offer guidance on how to navigate them effectively.

- Increased flexibility. As the demand for data continues to grow, it’s important that your business is ready to adapt to new regulations and requirements. By selecting a provider that is experienced in B2B integration, e-invoicing and tax reporting, you can overcome new hurdles without the need for a major system overhaul.

- Reduced risk. By streamlining tax clearance processes and automating e-invoicing workflows, a unified tax reporting and B2B integration solution can accelerate approval processes while greatly reducing the frequency of errors and delays.

- Audit readiness. With a single provider handling your business’s tax reporting and B2B integration processes, accessing accurate, jurisdiction-specific tax reporting and e-invoicing data is easy.

How ecosio and Vertex’s collaboration is changing the game

Remarkably, despite the numerous benefits that a unified B2B integration, e-invoicing and tax reporting solution offers multinational businesses, no such solution existed until August of 2024, when EDI and e-invoicing experts ecosio were officially acquired by tax compliance giants Vertex.

The result of this unique collaboration? An unparalleled global solution for indirect tax reporting, e-invoicing and compliance.

Instead of juggling multiple tools and platforms for tax determination, periodic transaction controls (PTC), continuous transaction controls (CTC) and electronic data interchange (EDI), businesses can now outsource all of these issues to a single provider for the very first time.

Via one connection, businesses benefit from the powerful combination of ecosio’s global network and powerful B2B integration technology and Vertex’s end-to-end Indirect Tax offering.

With a single connection you can now…

- Mitigate the risk of non-compliance

- Meet global CTC and reporting requirements

- Eliminate manual processes

- Accelerate revenue

- Streamline data extraction

- Ensure audit readiness

Want to know more?

For more details on how ecosio and Vertex’s collaborative approach could help you simplify and streamline your existing tax, B2B integration and e-invoicing processes, get in touch today.

Der Beitrag How to Manage the Growing Challenges of Tax Reporting, B2B integration and E-invoicing erschien zuerst auf ecosio.

]]>Der Beitrag What is Peppol and how does it work? erschien zuerst auf ecosio.

]]>- Peppol is a standardised framework for electronic document exchange, used for fast, secure, and compliant B2G and B2B communication

- Its four-corner model enables universal connectivity via a single certified Access Point, eliminating the need for custom EDI links

- Documents follow Peppol BIS standards, reducing mapping effort and ensuring compatibility across partners and countries

- API integration with Access Points like ecosio offers real-time tracking and ERP visibility, streamlining compliance and automation

With more and more governments worldwide mandating the use of e-invoicing for transactions involving public bodies, the use of Peppol is growing rapidly among supply chain businesses. As an ever-growing number of companies become Peppol-enabled, Peppol in turn grows increasingly attractive for those businesses not yet connected.

In this article we’ll answer some of the most commonly asked questions surrounding Peppol, how it works, and how it can benefit you.

Peppol basics

What is Peppol?

Peppol, which stands for Pan-European Public Procurement Online, is not an e-procurement platform. Rather Peppol provides the methodology and technical specifications as well as an agreement framework to send documents between e-procurement partners.

In short, Peppol makes it easier for businesses and public authorities to exchange electronic documents such as invoices and purchase orders in a standardised and secure way. It’s especially helpful for cross-border transactions, as it ensures documents are compliant with local regulations and can be processed quickly.

Why is Peppol popular?

Although theoretically governments could use any common communication protocol, such as SFTP, X.400 or AS2, this would require government bodies to support each one, which would involve significantly more work and increase the likelihood of errors occurring. Peppol solves this problem by offering a single, consistent framework.

Compared to document exchange via traditional EDI channels, Peppol also offers faster connections, reduced partner connection costs, increased message reliability and an all round simpler process for everyone involved.

Given these significant benefits, it’s hardly surprising that Peppol’s usage has grown steadily over the past decade. Today Peppol is not only used across the vast majority of European countries but further afield as well, with countries such as Australia, Canada, New Zealand, Singapore, the USA, Japan among others all now placing their trust in Peppol.

What are the three pillars of Peppol?

Ultimately, what Peppol provides can be boiled down to three factors, which are known as the three pillars of Peppol. These are…

- The Peppol network

- Peppol’s document specifications

- Peppol’s agreement framework

For more information on each of these pillars, please see the following three sections.

What’s required to connect to the Peppol network?

In simple terms, all a business needs to be able to connect to Peppol (in addition to the capability to send and receive automated messages) is a connection to a certified Peppol Access Point, such as ecosio.

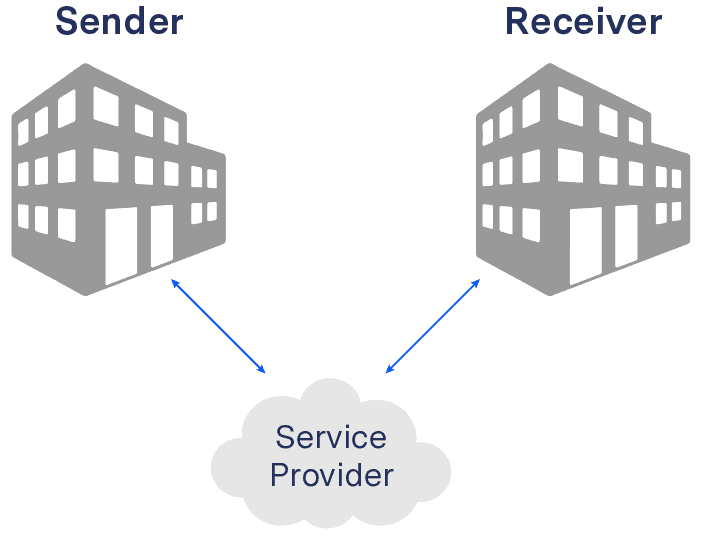

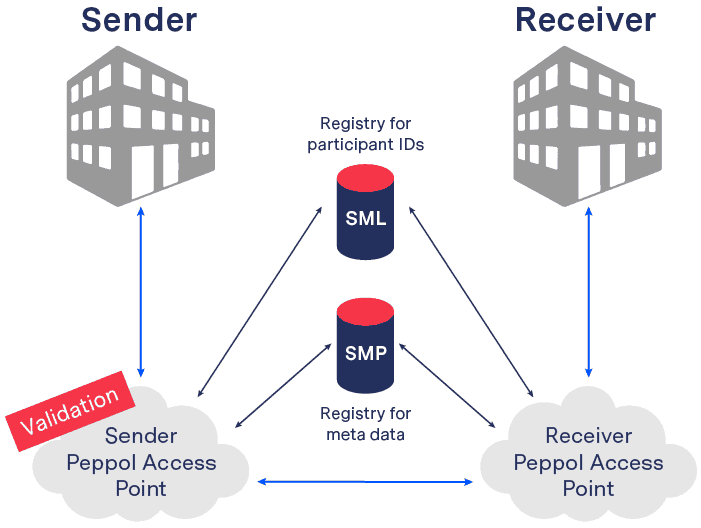

Whereas before Peppol, trading with partners may have required connections to several service providers, with Peppol this is not the case. To ensure exchanging key B2B data with partners is as simple and cost-effective as possible, Peppol uses a four corner connection model. Unlike two and three-corner models, this model means that a single connection to a Peppol access point is sufficient to exchange automated documents with any other Peppol-enabled companies.

The two-corner model

Also known as point-to-point transmission, the two corner model requires time-consuming set-up and is usually handled by inhouse IT teams. Due to the high maintenance effort and setup time this model does not scale well. As connections are not reusable for multiple partners, each partner needs a new setup.

The three-corner model

In this model message routing is done via a central hub offered by a service provider. The main downside is lack of flexibility, as both sender and receiver must have the same service provider, meaning it is badly suited to large supply chains such as those for which Peppol was created. In addition there is a ‘lock-in’ effect in regard to the service provider – i.e. one of the parties is usually forced into a contract with the service provider of the buyer or the seller (depending on the market dominance of the party).

The four corner model

This has several advantages over the two corner and the three corner transmission models. Unlike them, the four corner model offers simplicity and flexibility, allowing for quick and cost-effective connections to partners. To exchange information, sender and receiver aren’t required to set up unique point-to-point connections or use the same service provider.

Once a connection to an access point has been established, the Peppol Participant ID is sufficient to send an electronic message to any Peppol partner of choice. Vice versa, after connecting to Peppol a company can be reached by any other Peppol sender.

What are Peppol’s document specifications?

When it comes to the formatting of documents exchanged between Peppol Access Points, all messages must conform to Peppol Business Interoperability Specifications 3.0 (known as Peppol BIS). The Peppol Code list provides standards for >100 message types (most of which are Peppol BIS). Peppol also allows custom document types within a country, if these are officially acknowledged.

This way each access point only needs to be able to process these approved messages. Consequently, systems connected to the Peppol access point only need to convert from the BIS format to the inhouse format and vice versa. Thus, once the mapping is set up, it is valid for all business partners. This is much simpler than building custom mappings for each partner connection.

What are Peppol’s Transport Infrastructure Agreements (TIAs)?

Finally, the existence of Transport Infrastructure Agreements (or TIAs) ensures that all parties conform to the necessary Peppol regulations This protects the reliability of document exchange via Peppol. Peppol Authorities, Peppol Access Point providers and Peppol Service Metadata Publisher providers must all sign these agreements.

Peppol Access Points

What is a Peppol Access Point?

A Peppol Access Point is a software, offered or owned by a company, that can connect others to the Peppol network and exchange documents via the required standards/protocols and in accordance with the necessary regulations.

Why do you need a Peppol Access Point?

Apart from becoming a Peppol Access Point yourself (which involves several complex steps), connecting to a Peppol Access Point provider is the only way to get an officially registered Peppol ID, which all Peppol participants must have in order to experience Peppol’s benefits. Without an Access Point and a Peppol ID, exchanging automated documents with your business partners via Peppol’s international e-invoicing network is impossible.

Isn’t it easier to set up an EDI connection to my partner directly?

In short, no. As we explore in more detail in our introductory video on Peppol, Peppol hugely simplifies automated document exchange for connected companies. Instead of requiring you or your provider to build an EDI (electronic data interchange) connection to your partner from scratch, Peppol utilises a four corner model and enforces the use of specific standards and protocols, meaning there is less work required for each connection. This makes partner onboarding via Peppol faster and more scalable than via classic EDI.

How do I find a Peppol Access Point?

You’ve already found one! At ecosio we are e-invoicing and Peppol experts and can help you get connected to Peppol in no time.

A full list of all certified Peppol Access Points can also be found on the Peppol website.

How do Access Points differ from one another?

Although all Peppol Access Points will enable you to connect to Peppol, not all Access Points offer the same service. For example, the level of help provided by Access Points with regard to setting up new mappings and monitoring messages etc. varies wildly from one provider to the next. Further, some Access Points may be faster than others to adapt when Peppol introduces new technical requirements, such as the recent move from AS2 to AS4.

Different Access Points are also governed by different Peppol Authorities across the globe. While all are able to connect you to Peppol, it makes sense to select an Access Point that operates in the same geographical area to you.

Perhaps most significantly, however, very few Peppol access points provide APIs (Application Programming Interfaces) to help their customers achieve the best possible connection to their partners…

What are the benefits of connecting to Peppol via API?

Peppol as a whole has been developed to streamline B2G and eventually also B2B transactions. Conducting Peppol with the help of an API connection simply takes this streamlining to the next level (just as an API connection is able to boost the efficiency of traditional EDI).

An API basically specifies how different applications shall interact with each other, by defining the exchange format, exchange protocol, security requirements, etc. Thereby, APIs can help businesses connect their own internal IT landscape to other third party services. While Peppol perfectly solves the interoperability challenge between heterogeneous B2B networks by introducing a common exchange infrastructure, it does not define the “last mile”. As in telecommunications the last mile refers to the connection piece between the network hub and the end user’s system (e.g. the telephone).

In case of Peppol the network hub is the Peppol access point and the end user’s system is the ERP system of the company. The ERP system is usually the main system, where invoices, orders, despatch advices etc. are being created and consumed. If a Peppol access point provider offers a dedicated API, the ERP system can be seamlessly connected to the access point.

Using such an API for Peppol transactions comes with a number of significant advantages for the customer, including:

End-to-end message monitoring

With an API connection, Peppol can be seamlessly integrated in your ERP system. This enables users to see the delivery status of messages from within their existing user interface, eliminating the need to log into independent external software to check that a partner has acknowledged a message.

Accurate delivery/fetching of messages

Once connected to your Peppol access point via API, requests can be set up at regular intervals to check for new messages. Alternatively, new messages can be transferred proactively from the Peppol access point to the recipient.

Full text search

Thanks to the depth of the integration provided by the API, messages can even be searched directly in the ERP system. For example, users could locate invoice messages by inputting any relevant invoice data such as article number, reference to the underlying despatch advice, etc.

Error handling

Unlike with traditional protocols such as SFTP, where it can be difficult to ascertain where and why sending failed, thanks to the unparallelled data visibility achieved with an API connection, users can immediately see where the issue occurred and what should be done to resolve it.

How long does connecting to Peppol take?

Once you’ve chosen your preferred Access Point (something that should not be rushed), the actual connection process is fast and simple. Your provider will register a unique Peppol ID for you, whereby existing IDs such as VAT-ID or Global Location Numbers can be reused.. After this you will be able to start connecting to other Peppol-enabled partners and exchanging structured invoices etc.

Peppol in SAP systems

Is an SAP Peppol connection easy to achieve?

While achieving an SAP Peppol connection is very possible, its complexity depends on your chosen integration method. The simplest way to achieve an SAP Peppol connection is to opt for a managed service provider that will handle everything from technical setup to message monitoring and error resolution once the connection is live.

How does ecosio achieve SAP Peppol connectivity?

The illustration below shows a connection between an SAP System and Peppol with the help of ecosio. ecosio is a certified Peppol Access Point Provider and can therefore send and receive documents to and from the Peppol network.

The connection between the SAP system and ecosio occurs thanks to the EPO Connector. The EPO Connector is a middleware solution for SAP and entirely programmed in ABAP. The solution is SAP certified for all SAP versions from 4.6 and is thereby also compatible with S/4HANA. IDoc documents can be sent and received through the EPO Connector to the ecosio MessagingHub. For example, one can use INVOIC02 IDocs for e-invoices.

Should an SAP middleware such as SAP PI or SAP PO be the current solution, those components can also be used to connect to the ecosio MessagingHub. Additionally, SFTP solutions can be used for the connection as well. The SFTP server can either be hosted by ecosio or by the company.

After receiving the IDocs, ecosio will determine the sender, receiver and document type, and will convert the message to the correct target format, to finally transmit it to the receiver. If Peppol is in use, the delivery to the receiver’s Peppol Access Point will take place via the PEPPOL network, e.g. to German authorities or a company, which uses Peppol.

This allows for e-invoices to be sent via Peppol straight from SAP and be compliant with the XRechnung standard.

The communication is also possible the other way. For example, purchase orders can also be received over the Peppol network.

Why should you consider ecosio as your Peppol Access Point provider?

ecosio is one of a limited number of certified Peppol Access Point providers that offers Peppol connectivity as part of a comprehensive full service package.

With a single connection to ecosio, your business can trade all relevant e-documents with hundreds of thousands of connected companies and public institutions worldwide. What’s more, as we are able to handle all EDI and e-invoicing tasks for you, from set-up right through to ongoing operation, you don’t need any in-house expertise to benefit from the savings associated with automated B2B document exchange.

To find out more, get in touch today!

Are you aware of our free XML/Peppol document validator?

To help those in need of a simple and easy way to validate formats and file types, from CII (Cross-Industry Invoice) to UBL, we’ve created a free online validator.

SAP ERP and SAP S/4HANA are the trademarks or registered trademarks of SAP SE or its affiliates in Germany and in several other countries.

Der Beitrag What is Peppol and how does it work? erschien zuerst auf ecosio.

]]>Der Beitrag Germany Commits to Making B2B E-invoicing Mandatory erschien zuerst auf ecosio.

]]>This progressive move toward e-invoicing not only demonstrates Germany’s commitment to leveraging technology for economic rejuvenation, but also positions German businesses at the forefront of digital financial practices.

What does the Growth Opportunities Act aim to achieve?

The act aims to provide tax relief measures to facilitate growth in an economy that has struggled in recent times, with Gross Domestic Product (GDP) having fallen by 0.3% in 2023. In short, by passing this act, the German government hopes to make the country’s economic landscape more efficient, transparent and resilient moving forward.

What changes will the Growth Opportunities Act bring?

A pivotal component of the Growth Opportunities Act is the introduction of a new e-invoicing mandate for domestic business-to-business (B2B) transactions. This development represents a drive to streamline financial operations and reduce the administrative overhead associated with traditional paper invoicing processes. Although debates within the Bundesrat in November 2023 suggested a potential postponement, which would have extended the timeline for adopting electronic invoicing until 2027 for receivers, the initial schedule set forth by the German Ministry of Finance (BMF) will proceed as planned.

What is the timeline?

The timeline for the phased implementation of the e-invoicing mandate is as follows:

- 1 January 2025: All German businesses must be able to receive and process electronic invoices

- 1 January 2027: German businesses with an annual turnover exceeding €800k must issue their invoices electronically for domestic B2B transactions

- 1 January 2028: All German businesses must issue invoices electronically for domestic B2B transactions

What are the technical requirements?

To ensure a seamless transition, electronic invoices must adhere to the EN 16931 standard. However, businesses retain the capacity to negotiate the Electronic Data Interchange (EDI) standards used, provided mutual agreement is reached between invoice issuers and recipients.

Whilst Germany will eventually need to comply with the digital reporting requirement (DRR), as outlined in the European Commission’s VAT in the Digital Age (VIDA) proposal, the mandate is specific to invoice exchange between supplier and buyer and does not include a Continuous Transaction Controls (CTC) / centralised model.

How ecosio can help

For organisations preparing to navigate this change, understanding the specifics of the mandate and beginning the transition early can significantly mitigate the challenges associated with adopting new technological frameworks. Thankfully ecosio’s e-invoicing experts are able to support you as Germany embarks on this journey toward digitalisation.

ecosio.invoicing makes meeting country-specific regulations easy. Our state-of-the-art Integration Hub acts as a single gateway to connect your business to customers, tax administrations and other government platforms all over the world; enhancing automation, driving down costs and helping you to achieve compliance.

Find out more

For more information on ecosio’s unique EDI solution, please contact us at edi@ecosio.com or talk to our Sales team.

Der Beitrag Germany Commits to Making B2B E-invoicing Mandatory erschien zuerst auf ecosio.

]]>Der Beitrag E-invoicing in Romania erschien zuerst auf ecosio.

]]>E-invoicing in Romania: the story so far

The gradual implementation of B2B and B2G electronic invoicing in Romania first started to take shape back in September 2021, when the country’s Ministry of Public Finance published a draft on the enablement of B2G e-invoicing via an existing national system called RO e-Factura. RO e-Factura is an IT system for reporting, storing and downloading invoices through the ANAF (The National Agency for Fiscal Administration) server.

The implementation of e-invoicing via RO e-Factura took place during a pilot programme, created to test B2G e-invoicing within the system. E-invoicing became operational from 1 October that same year under Ordinance no. 120/2021, which regulated the e-Factura system.

By December 2021, the country was taking its first steps towards a nationwide e-invoicing mandate, with Order no. 1366/2021 from 5 November 2021 approving the technical specifications and basic elements of the e-invoicing format RO_CIUS nationwide. At this stage, B2G e-invoicing was optional for taxpayers, as was B2B e-invoicing, but solely under the condition that both senders and recipients of the e-invoice were registered in the e-Factura registry.

In January 2022 Romania announced a move away from the voluntary use of e-invoicing, stating that B2B taxpayers supplying high tax risk products – products which bring about a high risk of tax fraud and evasion – would be obliged to use electronic invoices using the RO e-Factura system from 1 July 2022.

Products which fall under the category “high tax risk” (i.e. susceptible to tax evasion) include:

- Fruit and vegetables

- Alcohol

- Construction materials

- Mineral products

- Clothing and footwear

In January 2022, Romania applied to the EU commission for a derogation in order to bring about obligatory e-invoicing via the country’s e-Factura invoicing system for all transactions carried out between taxpayers in the Romanian territory. In order to enforce mandatory e-invoicing, the country’s government requested authorisation from the European Commission to apply an exception to Articles 178, 218, and 232 of Directive 2006/112/EC on VAT.

On 1 July 2022 Romania announced that:

- Romanian taxpayers were obligated to issue e-invoices for B2G transactions via RO e-Factura

- Taxpayers supplying or receiving high tax risk products as part of a B2B arrangement would be obliged to use e-invoices via RO e-Factura

In June 2023, it was announced that the European Commission had published a draft authorising the implementation of mandatory B2B electronic invoicing in Romania from 1 January 2024. This authorisation will remain in place for three years (from January 2024 until December 2026) or until the ViDA (VAT in the Digital Age) proposal is adopted by the EU.

What is ViDA?

ViDA (VAT in the Digital Age) is a strategy put together by the EU Commission to ensure fair and straightforward taxation for businesses. It outlines how tax authorities can utilise technology to combat tax evasion and fraud, help organisations and ensure that current VAT legislation is appropriate and necessary for businesses operating in the digital age.

On 19 September 2023 a draft decree was published which stated that the shift to a clearance model in Romania will be pushed back to 1 July 2024. Between 1 January 2024 and 1 July 2024 Romanian taxpayers will need to send their invoice to the e-Factura platform within five days of issue.

Current Romanian e-invoicing requirements

At the time of writing, all Romanian companies supplying high tax risk products are mandated to issue e-invoices using the RO e-Factura system

As we’ve seen, since July 2022 there has been a mandate in Romania for all companies that supply high tax risk products to other businesses to use the national e-Factura infrastructure for the issuing of e-invoices.

Additionally, regulation changes are expected that will see obligatory e-invoicing for all Romanian businesses from 2024.

Upcoming changes

From 1 July 2024, there will be mandatory e-invoicing for all B2B transactions across Romania using the RO e-Factura system, in addition to the existing requirement for B2G e-invoicing and B2B e-invoicing for high tax risk products.

From the start of 2024 until this deadline, taxpayers will need to send invoices to the e-Factura platform within five days of issue.

How to prepare for the changes

Here’s a short list of what your business can do now in preparation for the changes to Romanian e-invoicing regulations…

1) Review your current resources

Before making any decisions as to your preferred e-invoicing solution, it’s important to conduct a thorough audit of your internal resources – both technical and human. When performing an internal inventory, ask yourself the following questions:

- On average, how many invoices is the company sending and receiving every month?

- Does our current e-invoicing solution depend on a few individuals with specific knowledge?

- How easily could our current e-invoicing solution be adapted to work with the RO e-Factura system?

- How informed are the relevant individuals on the upcoming regulatory changes regarding invoicing in Romania?

2) Avoid short term thinking

While it’s important to prepare your company and employees for the upcoming regulatory changes, it would be foolhardy to assume that these are the last e-invoicing regulatory changes your company will need to adapt to. In fact, e-invoicing requirements are only likely to become more complex as your partner network expands and governments introduce increasingly specific regulations.

To ensure you’re fully prepared for whatever changes might affect your business in the future, it’s worth selecting a flexible e-invoicing tool that is able to adapt to your specific needs. For those businesses without extensive in-house e-invoicing expertise, this almost certainly means outsourcing effort and responsibility to an external e-invoicing solutions provider such as ecosio.

3) Don’t leave it to the last minute

The implementation of a new e-invoicing solution can seem like an inconvenience that some businesses may be tempted to postpone. However, doing so only causes bigger issues later on. You’ll need to update your e-invoicing system at some point, and leaving it to the last minute means you have less time to fully evaluate the available options, and a much greater chance of choosing an ill-fitting solution.

For these reasons, we strongly recommend taking the time to investigate the best e-invoicing solutions for you as early as possible. As well as avoiding the unwanted disruption caused by leaving it too late, we’ve also found that companies who prioritise choosing their new e-invoicing tool in a timely manner reap many benefits from doing so – from saving time and money to reducing risk and boosting competitive advantage. Try to see the implementation of a new e-invoicing solution as an opportunity to enhance your current business strategy and boost efficiency moving forward.

4) Stay abreast of e-invoicing developments

E-invoicing regulations are constantly being updated the world over. As a result, staying ahead of the changes can seem like rather a daunting task. But don’t worry! With ecosio’s e-invoicing newsletter you can get global e-invoicing updates straight to your inbox. Simply enter your details and you’ll be among the first to hear of all the latest developments in the field as and when they happen.

Three things to consider when selecting an e-invoicing provider

When evaluating different e-invoicing solution providers, asking the following questions should help you determine which one is a good fit for your company:

1) Can they streamline the entire e-invoicing process?

While some e-invoicing solution providers, like ecosio, offer a fully managed service, others require companies to take on some of the internal tasks required to achieve a streamlined e-invoicing process themselves. Before committing to a solution, be sure to get a full rundown of exactly what the e-invoicing service is prepared to offer and how much additional internal work will be required from your team.

2) Do they provide an API connection?

By connecting to your EDI provider via API, it’s possible for invoicing data to be seamlessly and automatically sent to and from your internal accounting system or ERP. This significantly improves data visibility and accessibility for internal teams, in turn reducing the likelihood of errors occurring.

For more information on the benefits of such an approach, see our detailed article on the benefits of conducting EDI via API.

3) Are they a certified Peppol Access Point?

As compliance with Peppol is already a mandatory requirement in many countries, selecting an e-invoicing solution provider that is also a certified Peppol Access Point (as ecosio is) is important.

Without access to the Peppol network, you will be unable to meet e-invoicing requirements in many countries and will therefore need to enlist the help of another e-invoicing solution provider should you wish to do business in those areas in the future.

Conclusion

Hopefully this breakdown of e-invoicing in Romania has provided you with the information you need to prepare your team for the upcoming regulation changes.

To ensure you don’t miss any further updates, register now for the ecosio e-invoicing newsletter. You’ll get the latest e-invoicing news straight to your inbox!

Der Beitrag E-invoicing in Romania erschien zuerst auf ecosio.

]]>Der Beitrag What is an E-invoice and How Does E-invoicing Work? erschien zuerst auf ecosio.

]]>In this article, we’ll take a look at the development and functionality of an e-invoice, as well as the challenges and benefits of e-invoicing for companies.

Definition of an electronic invoice

So, what is e-invoicing? Let’s start with the definition of the electronic invoice according to the EU Directive (Directive 2014/55/EU of the European Parliament and Council from the 16th of April 2014 on electronic invoicing for public contracts), which states that invoice recipients in public tenders are obliged to accept electronic invoices.

Definition of an e-invoice: an “electronic invoice” is an invoice issued, transmitted, and received in a structured electronic format that enables it to be automatically and electronically processed;

This EU Directive is solely concerned with organisations which provide services for public procurement and issue invoices as part of these projects or undertakings. The invoice recipients, who in this case are public companies, are obliged to accept electronic invoices. According to the same EU Directive, there is no obligation for the invoicing party to issue electronic invoices, however individual states are free to tighten up these regulations when specific scenarios call for it. We’ve provided a comprehensive summary about this and the situation in Austria in our article, “EU Directive adopted for electronic invoicing in public procurement.”

While the structuring of data records through e-invoicing sits at the heart of the EU Directive and provides for further central elements that an e-invoice should contain, the situation from a tax point of view looks somewhat different. In regard to tax law requirements, there are country-specific variations which must be observed in order for companies to be legally compliant when using e-invoices for business transactions.

From a tax law perspective, the implementation of e-invoices is not a specifically technical implementation or indeed tied to a specific format; rather what is important is that a correct invoice is created from which input tax (for example, VAT) can be deducted.

The following are, among others, the required criteria:

- Authenticity of origin, relating to the certainty of the service provider’s identity and the identity of the invoice issuer.

- Integrity of the content

- Legibility – readable by humans

We will return to these points a little later in relation to the requirements for e-invoicing. As is already evident from the definition of an e-invoice, there are numerous different criteria that need to be complied with due to different legal requirements. Because of this, companies need to consider a range of legal principles, as well as country-specific regulations, in order to be fully compliant when using e-invoices.

An introduction to e-invoicing

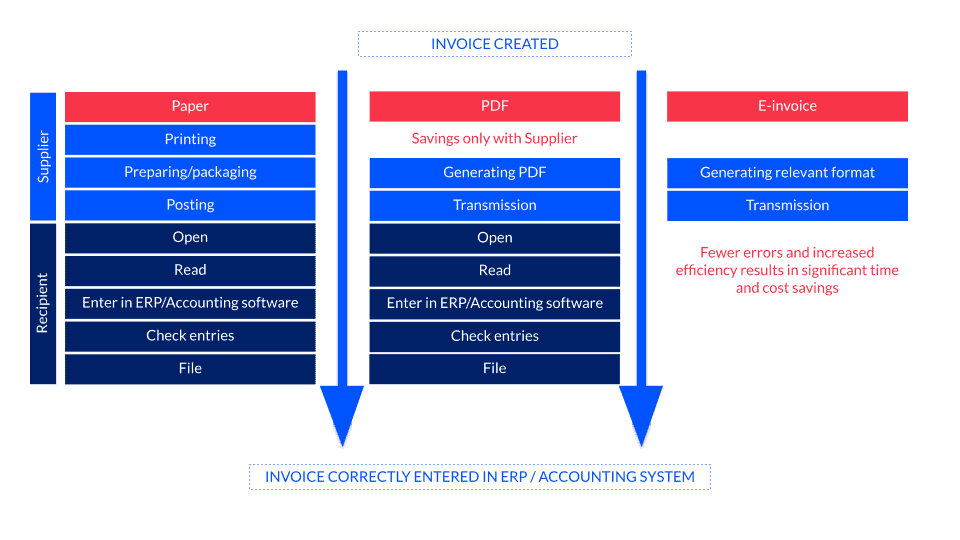

The beginning: paper invoices

Even today, many invoices are still sent as paper invoices. This is a questionable format to use due to its consumption of valuable resources and the costs incurred by both sender and receiver. Not only are there additional postage costs involved, processing invoices manually also brings about other costs, such as personnel and infrastructure expenses, which make the overall process considerably more expensive.

One step further: PDF invoices

After the paper invoice, comes the PDF invoice. PDF invoices have become increasingly popular since the discontinuation of the formerly mandatory electronic signature. This change means that PDF invoices can now be sent via e-mail or made available for download. Although in comparison to paper invoices, PDF invoices reduce the effort for the sender, due to the change in media, they do not significantly reduce the effort for the receiver. This is because PDF invoices can only be transferred to the recipient’s respective ERP/FIBU system manually or by using copy-paste, as the PDF format itself is unsuited to recreating machine-processable data. Formats which are better suited to this are XML and EDIFACT.

The e-invoice

Let’s look more closely at e-invoices and the significant changes that adopting this format brings about for those who use it.

What is an e-invoice in essence and what makes it different from the paper and PDF invoices which came before it?

In contrast to paper or PDF invoices, the e-invoice doesn’t require any manual input from users and instead enables a fully automated approach; e-invoices allow organisations to transfer invoicing information electronically, receive it automatically, and to have that information processed within the recipient’s own system.

Unlike other types of invoices, the e-invoice presents its contents in a structured and machine-processable format which enables automated processing. During sending, the e-invoice generates a machine-processable format which is sent directly to the IT system of the receiver. This occurs without any manual intervention from the receiver and from this point the invoice is ready to be processed further.

Comparison of invoicing methods

Using e-invoices / EDI invoices – challenges and requirements

Challenges in cross-border trading

Due to the country-specific formats and protocols which exist in relation to e-invoicing, there is a need for know-how and flexibility in cross-border trading, in particular relating to e-invoicing implementation. For many organisations, meeting the respective requirements needed to trade across borders can present something of a hurdle. It’s therefore important to evaluate if these challenges can be dealt with in-house, or whether it’s worth bringing in an external service provider with the necessary know-how to ensure a successful outcome.

In addition, the ViDA, issued by the European Commission, poses further cross-border trading challenges for companies.

VAT in the Digital Age (ViDA)

On December the 8th, 2022, the European Commission proposed a series of measures as part of ViDA (VAT in the Digital Age) to both modernise the value-added tax (VAT) system and make it more resilient against fraud. These measures were introduced in response to the loss of €93 billion in VAT in the EU in 2020. It is estimated that around a quarter of these losses can be attributed to VAT fraud in inter-community trade.

The European Commission has launched the “VAT in the Digital Age” initiative to improve the taxation of cross-border services and goods and adapt it to the challenges of the digital economy, in doing so closing loopholes and simplifying business procedures. The aim of the initiative is to ensure that businesses, in particular online retailers, make the correct VAT payments.

The following is an outline of the three main changes resulting from the ViDA:

- A new, real-time digital reporting system based on e-invoicing is to be introduced in 2028. In other words, e-invoicing is to become mandatory for all cross-border trading as of 2028.

- Updated regulations regarding VAT for the platform economy. Platforms for arranging passenger transport and short-term accommodation will be responsible for paying VAT to the tax authority, unless this is done by platform users themselves.

- Building on the existing “VAT One-Stop-Shop” model for online shopping businesses, VAT payments will be simplified for cross-border trade. Businesses will only need to register once for VAT purposes and will be able to fulfil all their VAT obligations through an online portal in a single language. This means that it will be sufficient for businesses to perform just one VAT registration when selling to consumers across the EU.

ViDA and electronic invoicing

ViDA aims to move towards real-time digital reporting based on electronic invoicing for companies that trade across EU borders. Key advantages arising from this include the reduction of administrative and compliance costs.

Compliance with the EU format is also addressed here. In cases where national e-registration systems are in use, they must support the EU format, which for electronic e-invoicing is EN16931. Business owners will need to bear in mind that the start of mandatory e-invoicing for cross-border trade has been set for 2028.

More information on ViDA (VAT in the Digital Age) can be found on the European Commission’s website under Taxation – Value added tax (VAT).

Ensuring the integrity of the invoice

As with previous invoicing formats, e-invoices are considered complete and unimpaired if the contents of the invoice have not been tampered with or altered in any way. However, this does not automatically mean that the invoice which has been issued contains the correct content.

Authenticity of the origin of an invoice

If the identity of the service provider or the invoice issuer can be guaranteed then the invoice fulfils the requirement for authenticity of origin. Authenticity can also be guaranteed through traceability.

Readability

The contents of each invoice should be fully legible and comprehensible. With e-invoicing, this can be facilitated through the use of the standardised messaging format.

Companies can choose to use one of a number of procedures to reliably meet the above criteria. However, as well as these requirements, there are, for example in Austria, the following additional e-invoice content requirements, which should also be taken into account:

- Name and address of the supplying company, or the company performing a specific service

- Name and address of the invoice recipient

- Quantity as well as description of the object of the invoice

- Date or time frame of services performed

- Invoice amount and tax rate

- Tax amount

- Date of issue

- Serial number

- VAT identification number (for invoices with an invoice amount of more than €10,000, the VAT identification number of the invoice recipient must be indicated)

In addition, depending on the type of enterprise, commercial law regulations also need to be observed:

- Legal status

- Registered office

- Company registration number

- Company accounts registrar

More information on this can be found in our blog article on the requirements of correct invoicing in Austria.

Furthermore, in Austria, additional content (such as the supplier number, order reference, etc.) must also be included, for example, when submitting an e-invoice to the federal government.

Archiving/Retention

It’s important to comply with retention periods for e-invoices. This applies above all to the tax office, which checks whether, for example, taxes have been paid correctly in Austria according to the Federal Tax Code. If the e-invoice has also been converted into another format, it must be clear from the retained file that no changes have been made to the document. For these reasons, it’s recommended to keep hold of both the original file and the converted file when possible.

Implementation of e-invoices

To ensure successful e-invoice processing and implementation, there are a number of additional aspects that need to be considered. Firstly, companies need to put in place workflows and systems for the creation and processing of e-invoices. Secondly, clarification regarding how e-invoices should be sent and received is needed. This clarification should pay close attention to country-specific regulations.

In addition to taking into account these requirements, there are also specific elements that the e-invoice itself must contain. The standard that specifies this was developed by the European Committee for Standardisation (CEN): EN 16931. Although this documentation provides useful recommendations for successful e-invoicing implementation, it only provides the fundamentals; each individual member state provides its own list of requirements, known as Core Invoice Usage Specifications (CIUS) to assist in the smooth implementation of e-invoices for businesses.

E-invoice standards and formatting

As we’ve seen, the CIUS only provides a basis for e-invoice implementation. Because of this, various versions of these have developed which has led to different e-invoice formats in different countries. This means that electronic invoicing can fall under different standards or specifications. In Austria, for example, the CIUS-AT-NAT was developed, while Germany has the XRechnung.

What exactly is regulated under EN 16931?

EN 16931 regulates core elements of electronic invoices, the requirements for which are syntax-neutral, i.e. prepared using plain or neutral language. However, the CEN does provide a list of permissible syntaxes (XML schemas) and we’ll provide concrete examples of those relating to the XRechnung in a later section of this article. What this regulation means for both sender and recipient is that for the e-invoice to be sent and received correctly both parties must be able to process the formats used.

How to send an e-invoice (using Germany as an example)

Different country requirements must also be taken into account when sending an e-invoice. In Germany, for example, there are two invoice receipt platforms (ZRE and OZG-RE) through which e-invoices can be transmitted to primary and secondary federal administration departments. For correct transmission, the sender must first determine which of these two platforms to use to send the e-invoice.

Various options can be used for the transmission of the e-invoice, with the type of transmission specified by each authority.

- E-mail & De-Mail (a German e-government communications service) with XML attachments

- Web entry

- Upload via an online form

- Fully automatic via Peppol

When invoices need to be sent frequently to federal government departments, it makes sense to use a fully automated transmission option via the Peppol protocol, which is supported by all authorities in Germany. In order to be able to transmit e-invoices via Peppol, a business will need a Peppol access point which can effectively communicate with the ERP system.

If the corresponding ERP system is already available in the company, it is worthwhile to convert an invoice in the respective ERP system into the necessary e-invoice format (e.g. XRechnung) automatically in order to transmit it immediately. To make this possible, there are fully automatic EDI solutions for the various ERP systems that can handle this conversion process. Through standardised import and export interfaces, the EDI systems can be integrated with the respective ERP system and therefore able to manage all electronic invoicing automatically.

When choosing the protocol, it is again important to consider which are prescribed by the country’s legislator.

How does e-invoicing work (using the example of XRechnung)?

Using XRechnung as an example, let’s now take a look at how e-invoicing works in practice.

As a mandatory e-invoicing standard in Germany, XRechnung affects all public institutions and authorities in Germany, as well as any companies that issue invoices to public administrators as clients. Suppliers, for example, must be able to create and send XRechnung invoices, while the authorities must be able to receive and process them.

Necessary steps:

- Clarify whether the company is legally required to create or receive the XRechnung (this varies from state to state).

- If so, implement the necessary e-invoicing standard in the company:

- Question current invoicing processes. How are outgoing and incoming invoices currently created and processed?

- If an ERP system is already in place, can it create or process electronic invoices?

Regarding the technical transfer of the XRechnung, according to the applicable standard, it must be transmittable or processed in one of the following two syntaxes:

a.) Universal Business Language (UBL)

b.) UN/CEFACT Cross Industry Invoice (CII)

Outgoing invoice – creating the XRechnung:

The relevant ERP system must create the invoice documents in the UBL or UN/CEFACT CII format. If this is not possible, the invoice must be converted to the required format. It is important that the conversion is automated and that the appropriate fields such as item description, identification numbers, units of measure, partner identification, etc. are maintained and can be converted accordingly. In addition, it is also essential that a receipt ID (called Routing ID in the XRechnung domain) is applied. Otherwise, the delivery of the document is at risk.

Incoming invoice – processing the XRechnung:

Before looking at importing an invoice via XRechnung, it is important to look at the workflow for approving and receiving invoices and to assess how well structured it is.The goal here is to convert XRechnung into a format that can be processed by the ERP system and to integrate the process seamlessly into that system. In addition to the format, the transmission channel (protocol) which receives the documents also plays an important role.

The various transmission options and the significance of the Peppol protocol are examined in detail in our white paper “Praxisleitfaden XRechnung und Peppol” (in German).

Verification of electronic invoices

As a general rule, companies should not send electronic invoices without prior verification. However, due to various legal regulations, there are differences in the criteria that need to be observed for successful invoice delivery. As mentioned above, most companies use an ERP system to map and automate processes. These systems can also export invoices in certain formats. However, these export formats are usually unable to meet the requirements for electronic invoices, making it necessary to convert or file them accordingly. Ideally, these conversions happen automatically, but this does not mean that the accuracy of the converted document is guaranteed. Various sources of error, for example, during input or directly during conversion, can lead to errors that need to be identified at an earlier stage. This is precisely where the verification of the e-invoice comes into play, so that these errors can be corrected earlier, long before the invoice is transmitted.

Verification can be performed in-house or by an external service provider. If a service provider is commissioned, it ensures that the e-invoice is transmitted to the relevant authority in accordance with the required standard.

Free online tool for validating Peppol and XML documents

Have you discovered our free online tool for validating Peppol and XML documents yet? It allows users to validate your documents according to EN 16931 (e.g. XRechnung), EHF, OIOUBL, A-NZ PEPPOL BIS3, CII Cross Industry Invoice, OpenPEPPOL formats, various UBL types, and many more.

Benefits of e-invoicing/EDI invoices

The use of electronic invoicing results in a number of advantages over traditional invoicing, although those benefits may vary slightly depending on several factors, such as the use of the transmission method. It should be noted that by cooperating with an external e-invoicing specialist, businesses can benefit from further advantages, depending on the specific services offered by the specialist in question.

Cost savings and efficiency gains in sending and receiving

Compared to sending and receiving paper invoices, electronic invoicing eliminates all costs associated with paper invoicing. The elimination of the manual paper process and automated invoicing process in the corresponding ERP/FIBU system also frees up the human resources involved in this workflow.

Reduction of material costs

The costs associated with paper, printers, postage, and more, are no longer a consideration.

Faster payment processes due to faster turnaround times

In contrast to paper invoicing, the time between sending and receiving an electronic invoice is significantly reduced. Once sent, the invoice reaches the recipient immediately. This significantly increases the probability of timely payments.

Minimising sources of error

By eliminating many manual processes thanks to automation, sources of error are significantly reduced.

Simplification of archiving

Archiving, which also plays an important role in invoicing due to the various retention periods required by law, is also simplified by e-invoicing. There is no need for a suitable room to store the paper invoices, nor is there any risk of invoices being lost in a fire. When invoices are archived digitally, they can be kept in electronic form and backups can be created.

Other advantages of using an external service provider in the context of e-invoicing include the following:

Technical compliance of e-invoices

External EDI service providers like ecosio ensure that e-invoices are fully compliant with e-invoicing requirements.

Cost savings through efficient and seamless automation

If an EDI service provider is contracted, then the automation of the invoicing process and the minimisation of manual processes is guaranteed, resulting in significant cost savings.

Flexible, scalable and future-proof

As experts in the field of electronic invoicing, EDI service providers make it possible to react quickly to changes in legal requirements, to scale invoicing processes if necessary, and make them future-proof.

User-friendliness

If the electronic invoicing process is integrated automatically into a company’s ERP system by the service provider, this enables companies to continue to work with familiar interfaces.

Zero hassle

Service providers such as ecosio further reduce complexity by enabling all invoicing processes to be handled via a single connection to the cloud. This means, regardless of the particular invoicing format or protocol, the stress and worry is taken out of the transmission and receipt of invoices.

The challenges of e-invoicing

E-invoicing, with its country-specific legal requirements and characteristics, not only poses challenges for companies when invoicing internationally, it also presents numerous hurdles when it comes to its technical implementation. Addressing this second challenge in particular will be of paramount importance for companies as having the correct technical integration is a necessary prerequisite for taking advantage of the many benefits e-invoices can bring about.

What this often means is that the switch to EDI invoices may initially involve increased costs to ensure its correct integration into a company’s system. However, over the long term these costs will turn into savings thanks to automation.